Introduction

When money is tight, applying for a credit line is often one of the last things on a person's mind. The first options that come to mind for most individuals are to use a credit card, borrow from friends and family, visit a bank for a standard fixed- or variable-rate loan, or search online for charitable groups accepting donations. If you ever run into financial trouble, pawnshops and payday lenders are options for you.

Corporations have relied on credit lines for decades to fund day-to-day operations and capture significant investment opportunities, but individuals have shown little interest in this form of borrowing. This could be because banks rarely promote credit lines, and many potential borrowers never even think to ask about them. A home equity line of credit is the only other type of credit line that can be borrowed against (HELOC). This is a mortgage loan, which presents its own set of difficulties and dangers. Here you’ll learn how a line of credit works.

A Line of Credit: What Is It?

If you get a line of credit from a bank or other lender, you can pay back the money whenever it's most convenient. Just as a credit card allows you to spend a predetermined amount of credit whenever and wherever you please, a line of credit is a predetermined sum of money that can be used as needed and repaid in a lump sum or over a specified length time. Good credit history and an established relationship with the lending institution are typically required for a line of credit to be approved by a bank. Remember that the interest rate is typically variable, making it difficult to forecast how much you will pay in interest if you borrow it.

Although lines of credit are a more secure source of income than credit card loans, the inflexibility of existing balances makes it more difficult for banks to manage their generating assets. They work to address the issue that traditional financial institutions are opposed to providing funding for short-term, unsecured personal loans. Financial sustainability cannot be achieved by the cycle of borrowing money every month or two, paying it back, and then borrowing again. A line of credit solves both of these issues by making a certain amount of money available to the borrower on an as-needed basis.

Circumstances Where a Credit Line Is Helpful

If the borrower has good credit and a history of solid money management, the bank may grant a line of credit for use in financing a significant, one-time purchase such as a house or automobile. The purpose of both commercial and personal lines of credit is the same: to smooth out fluctuations in monthly cash flow or to finance endeavours for which it is difficult, if not impossible, to accurately estimate the amount of money that will be needed in advance.

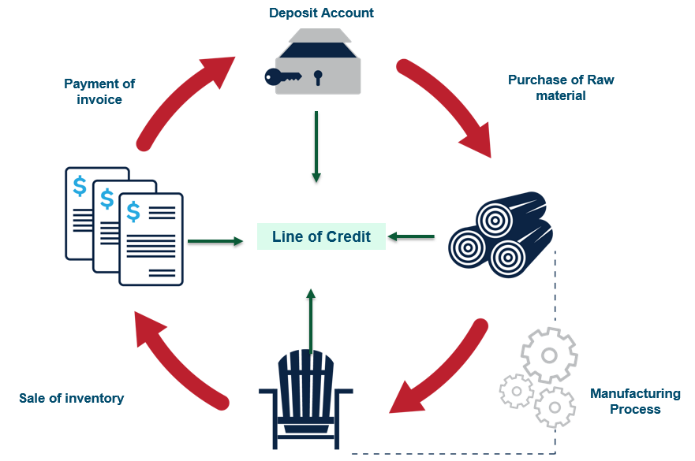

Consider the difficulties a self-employed person faces, whose income varies drastically from month to month or who must wait a long time before being paid for their services. A line of credit may be a better and more economical alternative than a credit card for this person because of the lower interest rates and more flexible payback options.

A line of credit is proper when you need to make a large initial cash outlay for an event like a wedding or when you'll need to make multiple smaller cash purchases, but the total amount of each is uncertain. During the housing bubble, many people took out lines of credit to pay for home improvements, which continued throughout the boom. Many homebuyers also take out a line of credit for renovations and maintenance after moving in.

Conclusion

The nature of credit lines is neutral, just like any other form of financial product. It's up to individual users to put them to the best possible use. However, just as reckless use of credit cards can lead to significant financial issues, so can reckless use of a line of credit. On the other hand, lines of credit can be convenient and inexpensive ways to deal with monthly monetary fluctuations or to carry out a complex transactions like a wedding or home improvement project. Money is a significant factor in these deals. Prospective borrowers should do their homework, not be shy about asking lots of questions, and pay close attention to the terms of any loan documents they are asked to sign (paying particular attention to the fees, interest rate, and repayment schedule).